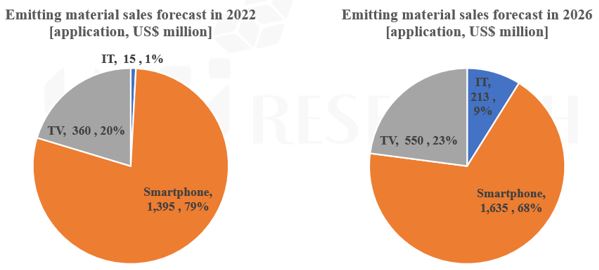

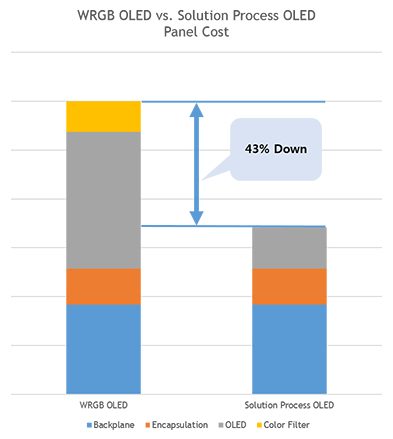

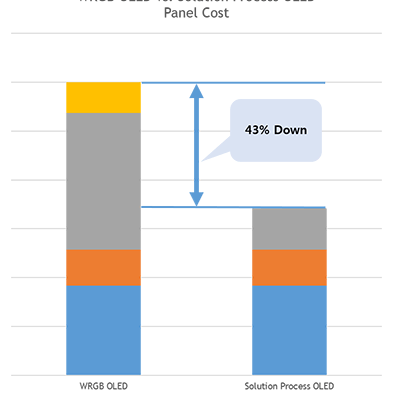

According to 2017 Solution Process OLED Annual Report published by UBI Research, when solution process (ink-jet printing) is applied to large area OLED, it could reduce up to 40% of component material cost, and approximately more than 18% of production cost compared to WRGB process that uses evaporation method.

Solution process is a technology that can manufacture RGB pixel structure of large size OLED panel without cutting mother glass using Gen8 manufacturing equipment or larger.

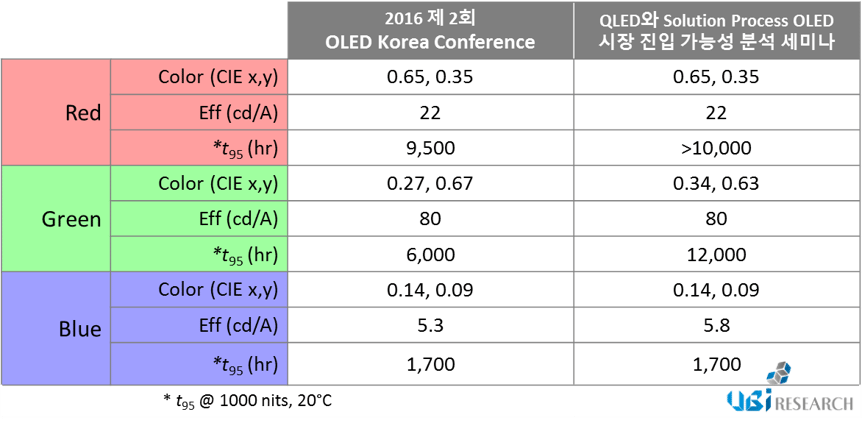

UBI Research analyst Hyunjun Jang explained that the solution process applied OLED has a simpler panel structure with 5 layers compared to 20 layers of WRGB OLED. WRGB OLED process material usage efficiency is only at 40% but solution process application could increase this to over 90%. Jang added that the lack of color filter is a factor that could decrease panel production price by reducing development cost. Particularly, this can greatly reduce emitting materials usage which occupies much of materials cost and contribute considerably to the fall in production cost. Furthermore, he added that cost setting of soluble emitting material per gram will be an important factor in production cost decrease and emphasized that organic material usage greatly decreases when soluble emitting materials are used but must consider price increase due to solvent cost, production cost, and development cost.

Solution process technology continues to receive attention as a key technology that can lead popularization of large area OLED, and key AMOLED panel companies are carrying out development.

In terms of technology, solution process OLED has lower emitting efficiency and short lifetime as diverse solvent is added to existing evaporation materials to transform into ink leading to low purity. This has been an important issue for panel and material companies for past several years. To improve this, DuPont, Merck, Sumitomo Chemical and others have been actively developing soluble OLED emitting materials. Much like evaporation materials, blue materials showed particular difficulty in performance improvement. However, at present significant portion of technology development has been carried out and investigation shows approximately 80% of lifetime and efficacy of has been achieved compared to evaporation materials.

2017 Solution Process OLED Annual Report compared and analysed WRGB OLED and solution process OLED’s competitiveness in terms of process, materials, and cost. Key issues, soluble OLED emitting materials development status, key companies’ trend, and solution process OLED market are analysed from various perspectives.

<Source: WRGB OLED and solution process OLED production cost comparison, UBI Research 2017 Solution Process OLED Annual Report>