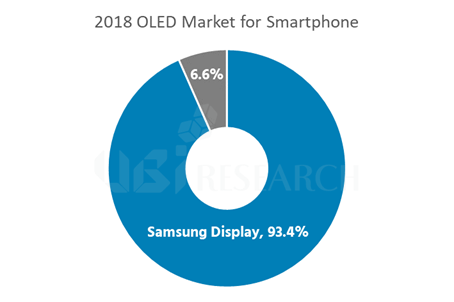

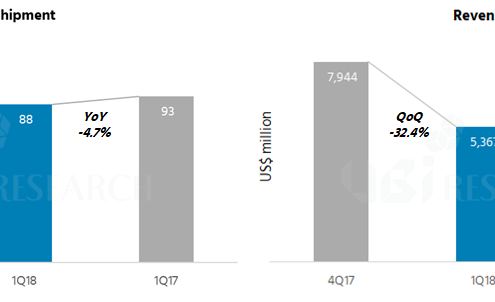

Samsung Electronics reported sales of KRW 62.05 trillion and operating profit of KRW 14.53 trillion through the conference call of the third quarter in 2017, and the display business recorded sales of KRW 8.28 trillion and operating profit of KRW 0.97 trillion. Display business sales increased 7.4% compared to the previous quarter and 17.3% compared to the previous year, but operating profit of 1 trillion fell with a decrease of 43.3% of the previous quarter and 4.9% the previous year. OLED sales are shown to occupy 60% of the display industry.

According to Samsung Electronics, in the 3rd quarter of 2017, main customers of OLED have increased through the launch of new flagship products focused on flexible products. However, its performance has decreased than the previous quarter due to factors such as increased costs of new OLED lines initial ramp-ups, and intensified price competition between rigid OLEDs and LCD panels.

Samsung Electronics plans to increase supply of flexible products in OLED in the 4th quarter, and expand sales of rigid OLED products to secure profitability. In the LCD industry, there are off-seasons and excess supplies resulting to supply and demand imbalance, but profitability is to be secured by strengthening yield and cost activities and expanding sales portion of high value-added products such as UHD, large-format, and QD.

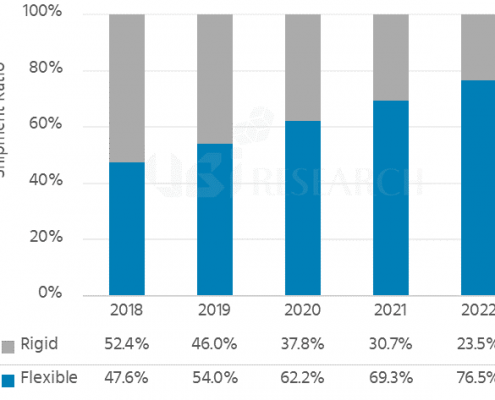

In 2018, OLEDs are expected to become the mainstream in the mobile display market, with expectations that flexible panel dominance will be particularly strong in the high-end product line. Samsung Electronics said it plans to develop a system to meet the flexible demand of major smartphone manufacturers and improve earnings by securing differentiated technologies.

In 2018, the LCD market may continue to expand in China and intensify competition among companies, but trend of large-sized and high-resolution TVs are expected to continue. Samsung Electronics states it will strengthen its strategic partnership with its customers and concentrate on improving profitability by promoting sales of high value-added products such as UHD, large format, QD, and frameless products.

Samsung Electronics sold 97 million mobile phones and 6 million tablets in the 3rd quarter of 2017. Mobile phone sales in the 4th quarter are expected to decline Quarter on Quarter, but tablet sales are expected to increase QoQ. TV sales reached a record around 10 million units, and sales in the 4th quarter were expected to rise to mid-30%.

10.4 trillion was invested in facility during the 3rd quarter of Samsung Electronics, of which 2.7 trillion was invested in display. Displays are reported to have additional production lines to meet customer demands for flexible OLED panel.

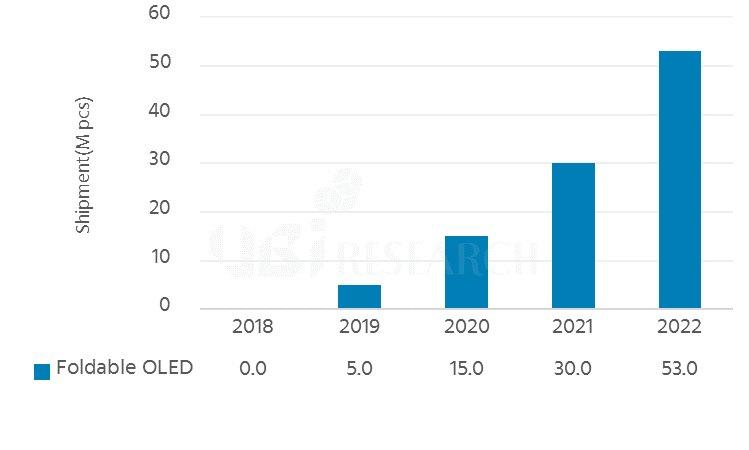

CEO Chang-Hoon Lee of Samsung Display said, “In the case of small and medium-sized OLEDs, we are planning to apply it to AR, VR, foldable, and automotive industry.” Also, “In Automotives, OLEDs are focused on energy efficiency, design differentiation, and black image quality which is critical to driver safety, in preparation with client company cooperation.” Additionally, “Foldable is constantly being researched and developed in line with customer demand, and is centered on enhancing the level of perfection demanded by the market and customers. We will work with our clients to prepare these for mass production desired by our customers.”

AMOLED 제조 공정 보고서 Ver.5 Sample 보러가기

AMOLED 제조 공정 보고서 Ver.5 Sample 보러가기